We take money for granted today in the United States. Our currency is standardized and federally regulated. A dollar in the bank, a dollar in your pocket, a dollar paid at the cash register. They’re all the same. It’s easy for us to forget that money didn’t always work this way.

I plead guilty to making mistaken assumptions about money when I’m researching the past. When I read that an item at the grocers cost a few cents in 1850, I assume that penny coins physically changed hands from purchaser to shop owner in order to pay for that item.

In reality, this was not typically what happened.

Cash in the Colonies

Cash was a huge problem in the British colonies. The economy was centered on shipping, and most of the money sailed away on merchant ships across the Atlantic. This left the cash-strapped colonists to make up ways to pay for the costs of everyday living. It was important for both the wealthy and the working class to establish trust within the community so you could get things on credit. If you had credibility, you could write an IOU, what they called “notes on hand.” If you needed something at the store, you were just given the items, and the shopkeeper kept a running account of what you owed. This was called book credit and you were expected to be pay your debts on a regular basis. Though payment might be in the form of bartered goods and services. Eggs and sewing were provided in exchange for sugar and rum.

Since British money was scarce, the colonists accepted a wide variety of foreign coins from across the Atlantic, with the Spanish silver dollar being highly popular. The Spanish dollar coin was often snipped into smaller halves, quarters, or eighths. There were also bills of credit, which were a kind of paper money unique to each colony. In the 1730s, Benjamin Franklin printed bills of credit for the Pennsylvania, Delaware, and New Jersey colonies. To thwart counterfeiters, Franklin innovated the use of distinctive inks, and the inclusion of colored threads and mica into the paper itself (Manukyan et al).

But, if you were traveling, you had to understand that the value of coins and paper money fluctuated. You could grab a local newspaper and check for tables that showed you the value of different money across the colonies. In 1775, for example, a Spanish dollar was valued at 6 shillings in New England, 8 shillings in New York, 7 shillings and 6 pence in Pennsylvania, but a whopping 32 shillings 6 pence in Charleston (Michener, “Money in the American Colonies”).

Money in the Early Republic

Surely things got better once the former British colonies formed the United States of America, right? Absolutely not. Many historians would argue that money in America became even more chaotic throughout much of the 1800s.

Alexander Hamilton had great visions of a rational currency controlled by a strong central bank. The First Bank of the United States was modeled after the Bank of England, which standardized the currency across the globe. Our new currency of U.S. dollars and cents was established under the Coinage Act of 1792. It was named after the familiar Spanish dollar, but it was based on a newfangled decimal system, which replaced the imperial pounds, shilling, and pence. This act also established a U.S. Mint in Philadelphia.

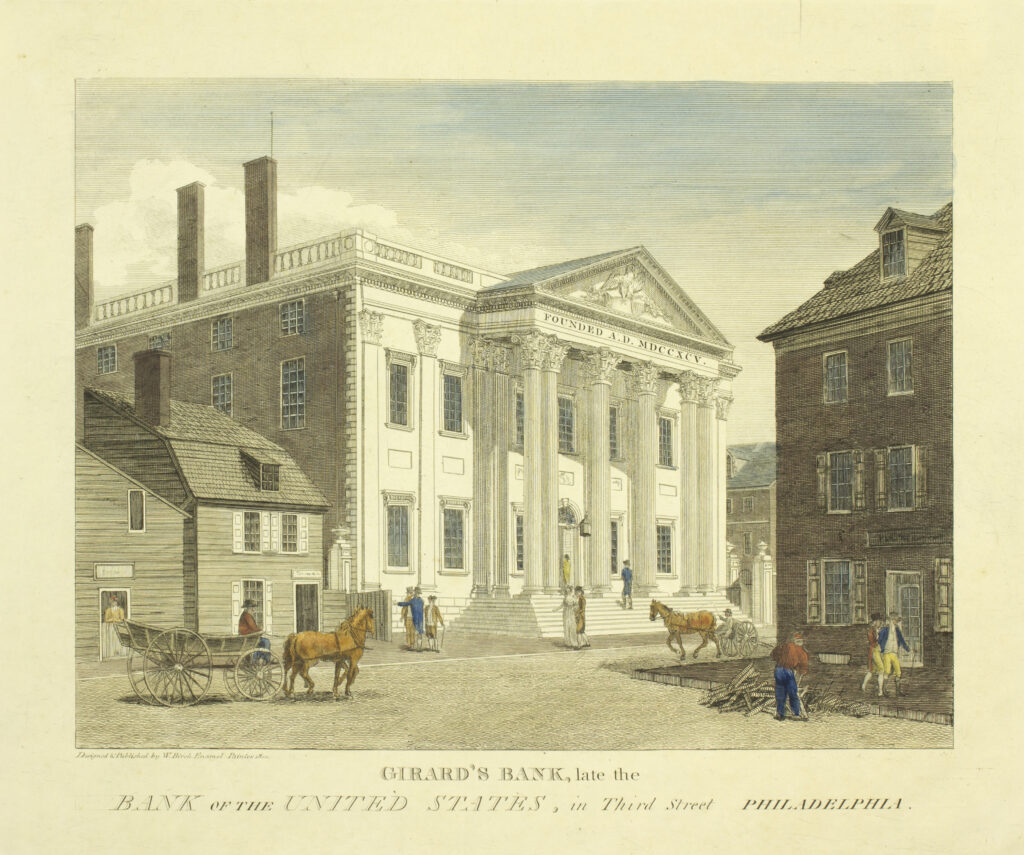

Hamilton’s plan was not a success. The bank proved to be political dynamite and it never was able to act like a central bank, though the building is still standing at 120 South 3rd Street. The U.S. Mint did produce coins, but at an anemic rate that could not keep up with the needs of a growing country. Foreign coins continued to circulate, along with the new U.S. coins. As late as 1849, a coin manual listed 850 different types of coins in use, with only a handful coming from the U.S. Mint (White, “Freedom’s First Con”).

And even the new decimal system was a hard sell. In 1820, John Quincy Adam noted during his travels throughout the country that people were still struggling to understand the new currency. Dollars were already familiar and mostly understood, but everyone was confused about cents. Despite living in a new, united republic, people were still paying for everyday goods using a variety of foreign coins, just as they had a hundred years before. It’s just that now they were being asked to value them in dollars and cents. Why bother? (Michener, “Money in the American Colonies”)

Fast, Cheap, and Out of Control

But the most confusing thing in this era was paper money. After the fall of the First Bank of the United States, the number of state-chartered banks exploded. The federal government tried to reign things in with the Second Bank of the United States from 1816-1836, but this bank also fell to political infighting. Though the massive building still stands at 420 Chestnut Street.

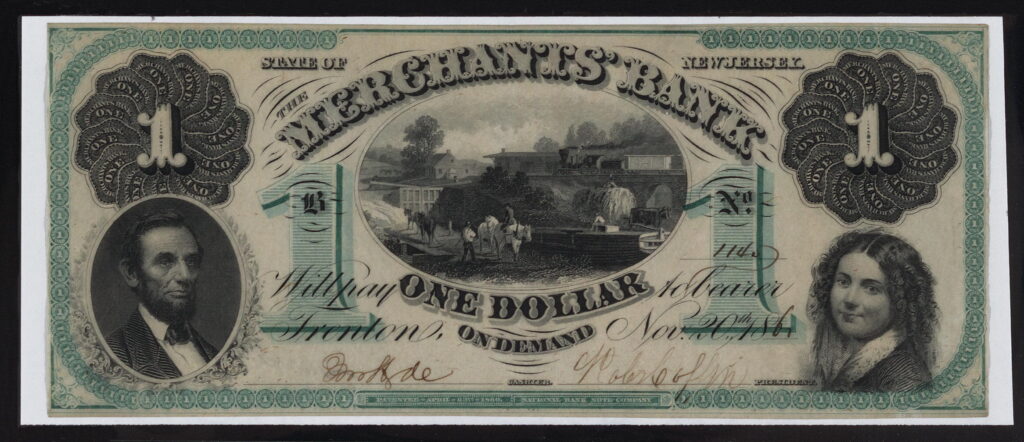

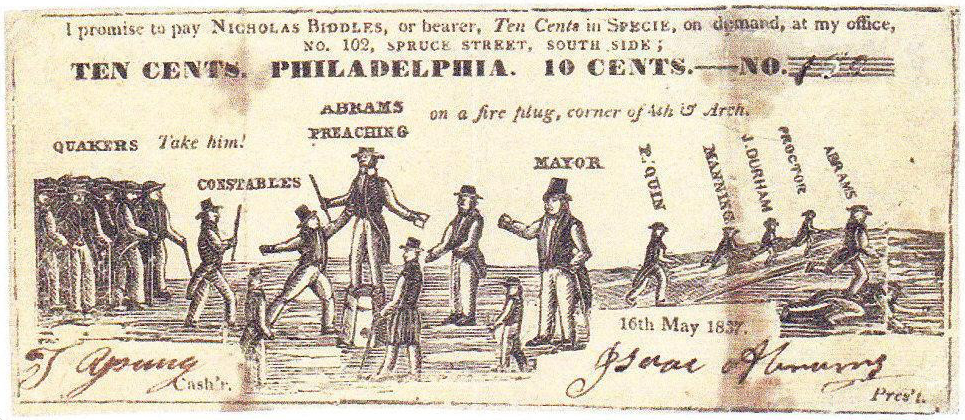

After its demise, small banks seemed to spring up everywhere in the 1840s. They were nicknamed “wildcat banks” and each bank was granted the right to print its own banknotes. The U.S. was awash in paper bank notes from an extraordinarily confusing number of banks. Here’s a few from later in the nineteenth century: The Merchants’ National of Chicago; The Merchants’ National of New Bedford, MA; The Manufacturers’ National of Amsterdam, NY; The Farmers’ National of Virginia, IL; The Farmers’ and Manufacturers’ Bank of Buffalo, NY. By 1860, 9,000 different paper bank notes were in circulation (O’Malley 72). Even small business owners started to print their own paper notes, called “shinplasters.” Barbers, druggists, grocers, and restaurant owners printed bills for amounts typically less than a dollar, which were given in place of change.

The chaotic paper money situation fueled a whole underworld of counterfeiting. This era was a perfect storm for shoddy banknotes, which fell along a continuum of dodgy-but-legal to outright counterfeit. There were genuine banknotes from banks that had failed; there were genuine banknotes from wildcat banks that had no assets and were considered worthless; there were genuine notes from solid banks whose denomination had been illegally raised. Then there were the counterfeit notes.

Many legitimate banks failed during these difficult economic times. When they were liquidated, counterfeiters would purchase the bank’s engraving plates at auction and use formerly-legitimate plates to print new counterfeit banknotes. Or the counterfeiters would mix plates from different failed banks to create entirely new and fictitious banknotes. A whole market of “counterfeit detector” publications was launched, claiming to help the average person keep track of this mess. One publication from 1890 helpfully explained the difference between a genuine and counterfeit two-dollar bank note from the National Union Bank of Kinderhook, NY: “On the genuine, the capital W in the words “Will pay to bearer” commences with a flourish, running on an angle with the first line of the W. On the counterfeit, the W commences with a flourish, forming an oval” (Dickerman 23).

The Paper Money Game

This is important. None of these pieces of paper money, even the genuine banknotes, was considered legal tender. The value of the banknotes fluctuated, typically decreasing the farther they moved from the home bank. People could, and did, refuse to take them. Every banknote was suspect with so much counterfeit money and questionable banknotes in circulation. Historians estimate that nearly 40 percent of U.S. money was counterfeit before the Civil War. People expected to receive a counterfeit note in their everyday exchanges. Every time money changed hands, Americans played a game where they tried to hold onto the banknotes from the most reputable local banks, and get rid of the dodgier, less valuable banknotes (O’Malley 7).

The exchange of money was an extremely complex social situation. You had to size each other up and decide how reliable the other person, and their money, was likely to be. Everything, from the dirt on their shoes, to the cut of their clothing, to the glint in their eyes, was under scrutiny. The power dynamic between the people making this exchange was critical. Exchanges of money were deeply unfair in an era where slavery was still legal in the south, and wealthy, white men were undisputed power figures in society. Factory workers and miners were paid in nearly worthless banknotes. Sailors were paid in banknotes printed far from their home ports. Illiterate Irish servants naively collected worthless shinplasters. The enslaved, running from slavery in the south, received dodgy or worthless banknotes in the north. This crazy, unregulated world of paper banknotes was cruelest to its least powerful members (Greenberg 56-71).

I’m thinking about turning this topic into a podcast episode. Let me know what you think at foundinphillypodcast@gmail.com

Bibliography & Works Cited

Dickerman, W. Dickerman’s United States Treasury Counterfeit Detector and Bankers’ & Merchants’ Journal. United States, W. Dickerman, 1890. View at Google Books.

Forret, J. “How Deeply They Weed into the Pockets”: Slave Traders, Bank Speculators, and the Anatomy of a Chesapeake Wildcat, 1840–1843. Journal of the Early Republic, 2019, 39(4): 709-736.

Greenberg, Joshua R. Bank Notes and Shinplasters: The Rage for Paper Money in the Early Republic, University of Pennsylvania Press, 2020.

Hartigan-O’Connor, Ellen. “‘She Said She Did Not Know Money’: Urban Women and Atlantic Markets in the Revolutionary Era.” Early American Studies, vol. 4, no. 2, 2006, pp. 322–52.

Manukyan, Khachatur, etal. “Multiscale analysis of Benjamin Franklin’s innovations in American paper money.” Proceedings of the National Academy of Sciences, July 17, 2023, 120 (30).

Mihm, Stephen. A Nation of Counterfeiters. Harvard University Press, 2007.

O’Malley, Michael. Face Value : The Entwined Histories of Money and Race in America. University of Chicago Press, 2012.

White, S. “Freedom’s First Con: African Americans and Changing Notes in Antebellum New York City.” Journal of the Early Republic, 2014, 34(3): 385-409.